“Pennies don’t fall from heaven, they have to be earned here on earth”

Margaret Thatcher, Lord Mayor’s Banquet, 12th November 1979.

We believe that many of the favourable conditions that have propelled markets for the last several decades are fundamentally changing for the worse, and that the equity market as a whole look highly concentrated and fully valued. Paradoxically, at the same time we see there are opportunities selectively to acquire high quality income names at attractive prices, as they languish out of favour when set against the bright lights of technology/AI related stocks. In this update, we look at the changing market backdrop in the context of what has gone before, and at AI and valuations, and show how your portfolio sits in comparison. We end the piece with an illustration of the opportunities available by looking in detail at the merits of 3 recently acquired holdings.

Reverse Berlin Wall

Looking back to the fall of the Berlin Wall in 1989, it is very clear that a chain of events was set in motion that were very beneficial to the global economy and capital markets. Inflation and bond yields peaked around that time, as vast pools of cheap labour became available from behind the Iron Curtain. Under willing US leadership, the world was kept in a peaceful cadence (outside the Middle East) and globalisation was the dominant global economic force. This allowed companies to optimise their cost base and countries their competitive advantage.

This gained further momentum as China acceded to the World Trade Organisation in 2001 tapping a further pool of cheap labour. Following the global financial crisis, interest rates were dropped to 0% and experimental monetary policy was enacted in the form of quantitative easing. Taken together, the result has been a long and very rewarding bull market in equities (and until recently bonds) that has delivered exceptional returns to investors.

Today, this long ascent leaves investors with multiple risks to navigate. In big picture terms, much of the above is changing. The world is once again dividing into two spheres of influence, conflict is endemic, supply chains need to be realigned, and geopolitical pressures and tariffs look set to trump (no pun intended) the optimisation of capital. Inflation has returned and bond yields have risen. The losers from globalisation have become increasingly vocal via the ballot box leading to a fractious and unstable political environment across the world.

Notwithstanding this, equities (albeit following a wobble in 2022) have continued their climb leaving an economy and equity market inherently fragile. Stock market valuations are markedly high. The cyclically adjusted price-earnings ratio for the S&P 500 Index is now at 40x,1 a level not seen since the dot-com boom in 2000. The recent advance has been very narrow, driven primarily by those companies that are perceived as beneficiaries of current artificial intelligence (AI) spending, and to a lesser degree, deployment.

AI AI Oh…

The sums involved in the build-out of this technology are vast and are based on a heroic premise; that more spending will deliver more computing power that will in time lead to the development of artificial general intelligence with potentially miraculous (and terrifying) implications for the economy and society. The prize is deemed to be so great, and the cost of being left behind so existential, that no restraint on the spending of shareholders’ capital can even be contemplated. What is most remarkable is that the more companies spend, the more they are cheered on by investors, in stark contrast to the financial long face that usually greets unexpectedly high capital expenditure plans.

In the real world (or as one might say on earth) the risks are more prosaic – will the companies achieve a satisfactory return on investment in the foreseeable future? In a recent note, “AI Capex – Financing the Investment Cycle,” JP Morgan estimates that to achieve a 10% return on the AI capital expenditure projected by 2030, companies will need to generate $650bn of revenue. They suggest this is equivalent to $400 per year from every iPhone user. When framed in this way it is apparent this is a huge task even if AI proves to be a transformative technology. It is also changing the business models of many of the index’s largest and best performing companies. As one of our research providers Gerard Minack put it, “the investment torrent is transforming celebrated capital-lite companies into utility-like capex-hogs”.2

Further uncertainty derives from China which through necessity, owing to trailing in the production of the most advanced chips and unable to import US chips owing to export controls, seems to have been able to achieve similar results with dramatically less need for compute (the so-called “Deepseek moment”). This innovation, together with a willingness to pursue a more open-source model for technological development of AI undermines some of the arguments for the necessity of such vast spending.

If the need for the spending and the likelihood of return can be questioned so too can the source and deployment of that capital. Having been largely equity-financed until recently, companies are increasingly turning to debt finance, in various forms, to sustain spending. Much is also being done in a “circular” way in the sense that companies are either investing in, or lending to, others to maintain demand for their own products. This is surely a warning sign.

Should this spending be called into question the knock-on effects could be severe. This stems from the fact that the capex boom is propping up the US economy and the consumer via the stock market. This is already apparent as spending by the wealthier cohorts of US consumers has remained more robust than that of the less well off who do not benefit from asset ownership and suffer more severely from the effects of inflation. Hence a pause in AI capex, leading to a fall in the stock market would be a double blow to the economy. This should not be underestimated; a recession can be caused by a falling equity market rather than the other way around, as we saw at the turn of the century.

Concentration Risks

For investors the effect may be especially acute given the large proportion of global indices represented by technology companies. As described in Troy’s recent Investment Report no 86:

“At that time, as is the case today, there was a bias to invest based on size, not on value. This has worked well in recent years as the growth in passive investment bears witness. But are investors fully aware of the risks embedded in index funds? Do they provide prudent diversification or are they merely buying what has done well? Today, the largest 10 stocks in the S&P 500 account for over 40% of the index – a higher concentration than at any point in well over a century, eclipsing the >25% peak in the year 2000, and even the c.38% reached in 1900 at the height of the railroad era. Investors may believe index funds offer diversification, but when leadership is so narrow and correlated (emphasis added), that assumption deserves re-examination.”

At Troy we put a premium on assessing downside risks and seeking to protect investors from steep losses. We adhere to conservative principles such as building a diversified portfolio of high-quality companies that generate consistent growth in free cash flow, offer a steady and growing income stream and maintain discipline on valuation. We also try to avoid companies with overly optimistic growth expectations.

We aim to provide investors with income that can help cover some day-to-day expenditure, reducing the need to plunder their capital at times of stress. The fact that these historic virtues have delivered less reward than more aggressive approaches in recent years makes it more, not less, likely that they prove rewarding in the years ahead.

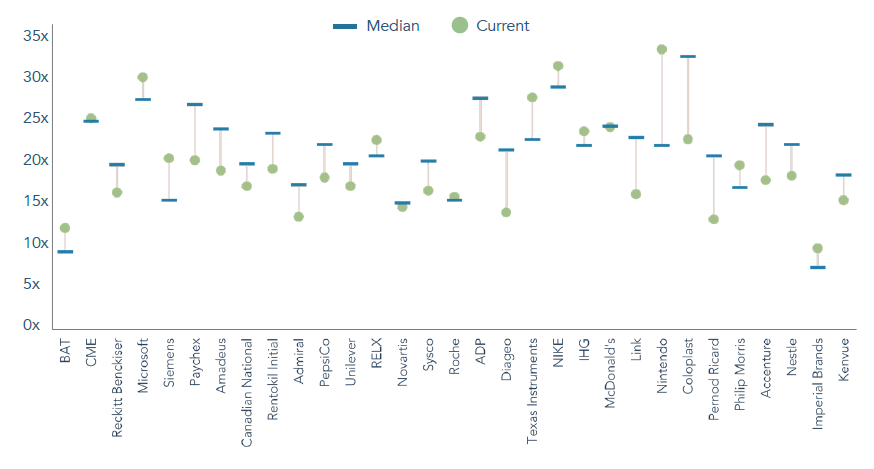

This is especially the case given that we are at a time when index levels of valuation are so rich, many of our portfolio companies are trading towards the lower end of historic valuation ranges (see chart below).

FIGURE 1 – MAJORITY OF PORTFOLIO COMPANIES ARE TRADING BELOW THEIR 10Y P/E MEDIAN

Source: Troy Asset Management Limited and Bloomberg, 31 October 2025. Past performance is not a guide to future performance. Illustrations are not representative of the entire portfolio. The reference to specific securities in this slide is not intended as a recommendation to purchase or sell any investment. Price-to-Earnings (P/E) ratio is a valuation metric that compares a firm’s stock price to its earnings per share. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Income Strategy.

The benefits of income investing

Income investing is at heart a “bird in the hand is worth two in the bush” approach. Companies that pay a regular dividend tend to be stable and mature which in turn reduces surprises and precludes rapid but perhaps unsustainable growth. The payment of a dividend offers a certainty of return as well as a conservative attitude to external financing and internal capital allocation. We are living through an age where capital is being deployed towards AI at a scale and at a rate that has never been seen before. This could be viewed as highly speculative at the macro level and potentially highly damaging to some of the best companies that have ever existed at the micro level should returns disappoint and capital intensity materially increase. After all the spending is certain, the return is most certainly not.

That this is taking place while valuation and index concentration is at levels rarely seen in history, and at a time of great geopolitical change, increases the stakes further still. For those of a more cautious disposition, now may be a good time to redeploy some capital gains into a more conservatively managed fund which delivers a secure a growing income stream. In doing so, investors may help shield themselves from the manifest excesses that we see in today’s market.

Meanwhile, under the surface, the market is giving us opportunities to invest in the type of companies we favour at attractive valuations. While others are falling over themselves to allocate more and more capital to the AI theme, we are selectively embedding greater quality and value in the portfolio. We illustrate this with short profiles examining 3 recent new holdings: Siemens, Nike and Sysco.

Siemens

Siemens is one of the largest industrial automation and electrification companies in the world. Siemens built its advantage by delivering high quality solutions (German engineering) over many decades, resulting in a large installed base. Industrial companies are risk averse and incumbents often win business, which confers Siemens a strong competitive advantage. Furthermore, the company has shown through the years good strategic foresight by investing early in Industrial software.

Today, Siemens is the largest industrial software company in the world, enabling it to capture more business as digital capabilities become increasingly important. The company continues to invest in its technical capabilities by spending 8% of its sales on research & development, more than some of its closest competitors. It is a clear beneficiary of some of the long-term trends such as electrification, decarbonisation, smart buildings and industrial automation.

The company is simplifying its corporate structure by spinning off its energy and healthcare subsidiaries Siemens Energy and Siemens Healthineers. We believe this restructuring will create value for shareholders, as we have seen with similar corporate restructurings at companies such as GE in the US. The remaining, more focused entity will benefit from a higher return on invested capital, improved margins and faster growth, supported by a debt-free balance sheet.

In November we attended the company’s Capital Markets Day in Munich which confirmed to us that the company is on the right track. Although the shares fell on the day, owing to a slight downgrading of expectations relating to foreign exchange and a lightly lower margin than expected, the strategic direction is clear.

We would expect future growth to exceed its conservative sales guidance of 6-9% translating into high single-digit earnings per share growth. We believe an unlevered 20x earnings therefore remains attractive and is a material discount to many peers. Siemens is a promising long-term investment with the prospect of a double-digit expected return should the company continue to progress as we expect.

Nike

Bought at the depths of the Liberation Day sell-off in April this has all the hallmarks of a classic long-term global income investment. The company has been a reliable compounder for a long time, with stable and gently rising sales and earnings, participation in growing markets, and a dominant position. The last five years have been anything but stable. The combination of strategic mistakes under the previous CEO and Covid-related distortions led to unsustainable sales and valuation at the end of 2021. As if this was bad enough, owing to a large footprint in Vietnam, the share price was especially badly hit on the day the tariffs were announced. This provided us with the opportunity for which we had been patiently waiting. At purchase the shares had fallen c. 70% from their peak.

The problems included a loss of product focus as the company moved away form its core sport-specific category structure to a more generic mens/womens/kids “consumer construct”. The resultant loss of experienced talent stalled innovation and dynamism in the company. Too much emphasis was also given to the direct-to-consumer channel at the expense of wholesalers. This soured relationships with retail accounts and diminished the Nike footprint in physical stores allowing other brands to have the oxygen to become established causing Nike to lose market share.

Nike is now once again finding its feet under new leadership of Elliot Hill. Hill is a Nike insider steeped in the company’s traditional playbook for product innovation and marketplace management. His mandate is to “return the struggling athletic brand to its glory days”. Along with the CEO change, Nike has been pruning costs – including layoffs of ~2% of the workforce – to remove bureaucracy introduced under the previous CEO. With a nimbler organisation and a refocused strategy, Nike’s leadership is emphasising a “back to basics” approach: make innovative products, inspire consumers with brand storytelling, and execute at retail with the right partners. The balance between long-term brand building and quick-turn digital marketing is being restored. Internally, there’s a cultural push to rediscover Nike’s competitive edge – reconnecting designers with athletes and customers, and reviving the risk-taking ethos that produced icons like the Air Jordan and Air Max. While the turnaround is still in early stages, Nike’s moves to course-correct – slimming down the lifestyle excess, reorganising around sports performance, and re-engaging wholesale – are setting the foundation for recovery. The company also halted its earlier pullback from wholesale – no further account cuts – and instead is using partnerships (e.g. Foot Locker, Dick’s, JD Sports) to ensure broad availability of Nike performance products. This omni-channel approach is aimed at recapturing market share and connecting with consumers wherever they shop.

While such volatility in a previously stable and predictable business is unwelcome, it should not be a disqualifying factor. Quite the opposite; if such a company has a big but ultimately fixable problem, it allows income investors such as us, to do what we are always aiming to do. To buy good businesses when they are out of favour.

The brand remains strong, and the company is now working hard to clear excess inventory, align supply with demand and go back to the roots that made Nike the largest sportswear company in the world. While we do not know exactly how the next few months or quarters will unfold, we are excited about the long-term prospects for this reinvigorated top-class company.

Sysco

Sysco is the world’s largest foodservice distributor, holding ~17% share of the U.S. market. The company leads the fragmented ‘food-away-from-home’ industry, where the top 3 players collectively hold ~31% of the market. The company enjoys substantial benefits of scale and generates twice the sales of its nearest competitor. This scale translates directly into superior purchasing power and superior gross profit margins in the US (~19.3%) which exceed the peer average by roughly 30%. Additionally, scale provides logistical benefits, allowing Sysco to efficiently serve geographically dispersed national chains. Moreover, higher route density enables a lower cost per delivery and the capability to stock a broader product inventory.

Sales are split 81% in the US and 19% International. In the company’s 55-year history, there have been only three years when sales did not grow year on year, the first was during the global financial crisis, the others were during the two years of the COVID pandemic when the food-away-from-home industry was decimated for two years.

Since 2016, Sysco has executed a major business transformation – improving efficiency, expanding globally through acquisition, and refocusing on higher-margin segments – and has navigated the 2020 COVID-19 shock emerging with renewed growth.

More recently Sysco has experienced slower-than-anticipated growth in independent restaurant case volumes, a key performance metric, which has caused investor concern. In response, management has intensified investment in salesforce capabilities and specialty-focused selling initiatives aimed at regaining local market momentum.

Overall, we see Sysco is well-positioned as an industry leader to generate mid-single-digit growth and robust cash flows, provided it continues to deliver on strategic initiatives. Recent concerns allowed us to establish an investment at an attractive valuation providing a solid entry point to allow for the long-term compounding of capital and income.

12th November 2025 marks the five year anniversary since Troy was entrusted with the management of STS Global Income & Growth. We thank our shareholders for their support.

1 Bloomberg

2 Companies or industries that spend significant amounts of money on capital expenditure (capex)

Please refer to Troy’s Glossary of Investment terms here. Performance data relating to the NAV is calculated net of fees with income reinvested unless stated otherwise. Past performance is not a guide to future performance. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the Trust’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Tax legislation and the levels of relief from taxation can change at any time. The yield is not guaranteed and will fluctuate. There is no guarantee that the objective of the investments will be met. Investment trusts may borrow money in order to make further investments. This is known as “gearing”. The effect of gearing can enhance returns to shareholders in rising markets but will have the opposite effect on returns in falling markets. Shares in an Investment Trust are listed on the London Stock Exchange and their price is affected by supply and demand. This means that the share price may be different from the NAV.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained within the Investor disclosure document the relevant key information document and the latest report and accounts. The investment policy and process of the Trust(s) may not be suitable for all investors. If you are in doubt about whether the Trust(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Ratings from independent rating agencies should not be taken as a recommendation.

Please note that the STS Global Income and Growth Trust is registered for distribution to the public in the UK and to Professional investors only in Ireland.

Issued by Troy Asset Management Limited (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP . Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training.

© Troy Asset Management Limited 2025